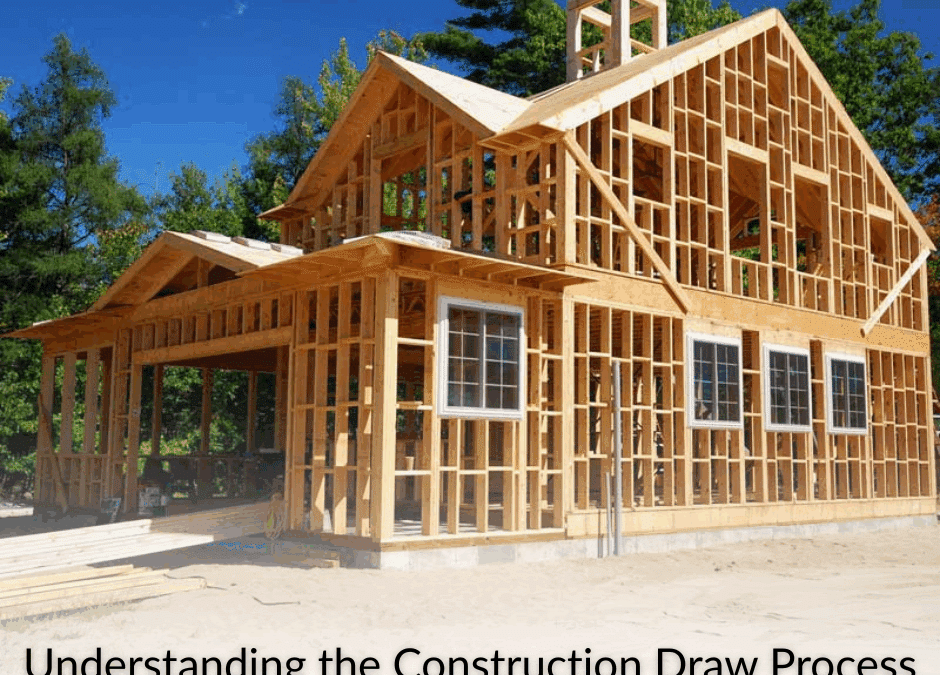

If you’re a real estate investor or builder looking to finance a project from the ground up, a hard money construction loan can be a smart move. These private loans offer fast, flexible terms, giving you the capital to acquire, build, or renovate without the delays and red tape of conventional financing. They’re designed for investment or business use and are secured by residential or commercial property.

With any construction loan, including hard money construction loans, funds are disbursed gradually as construction is completed or the project hits specific milestones, like site prep, framing, roofing, or interior work. To get disbursements on the loan approved, borrowers must submit construction draw requests. Knowing how the construction draw process works and how to manage the budgets and draw requests can be the difference between a smooth build and a stalled site.

At Cetan Funds, we specialize in fast, flexible residential construction loans and commercial construction loans across Oregon and Southwest Washington. We know how to meet the needs of builders and developers to help make this process as straightforward and easy as possible. In this post, we’ll explain why learning the construction draw process is important, answer some of the common questions, and explain how our approach helps keep your project moving forward.

Why the Construction Draw Process Matters

The construction draw process is the way you, the builder, get access to your funds, reimburse yourself and cover your expenses throughout the project. By releasing funds as work is completed, the process helps reduce costs and lower risk for both the lender and the borrower while keeping both parties on the same page regarding what’s been completed and what’s next. In addition to controlling costs, this structure keeps everyone accountable and ensures the project moves forward.

Before starting a construction project, the borrower should plan ahead with a preliminary draw schedule. This helps to manage cash flow, further reduce risk, build trust and mutual understanding with the lender, and prevent potential delays by aligning expectations.

Key Components of a Draw Schedule

Every project is different, but most draw schedules will include the following elements:

- Project Milestones: Funds are disbursed as work is completed so try to anticipate when specific milestones will be reached, such as demolition, site prep, foundation, framing, roofing, interior work, mechanicals, and finishes.

- Draw Requests: To access funds, borrowers submit draw requests with supporting documentation such as a breakdown of expenses, invoices, receipts, and photos.Clarify upfront what documentation the lender requires.

- Approvals: The approval process can differ from one private money lender to another. At Cetan Funds, borrowers work directly with their loan officer, their main point of contact from start to finish on the project, to submit draw requests. Loan officers review draw requests and typically issue funds within 24–48 hours. Cetan Funds allows up to two draws per month and tailors the process to each project’s scope.

Frequently Asked Questions

Below, Cetan Principal and COO Zach Smith and Cetan Associate and Loan Officer Landon Matta answer some of the most common questions we get about the construction draw process.

Zach Smith personally oversees loan origination, underwriting, and servicing, making him a trusted authority on construction financing in Oregon. With years of hands-on experience as both a lender, real estate investor and entrepreneur, Zach understands exactly what borrowers need to succeed.

Landon Matta works hard out in the field every day with Cetan clients, reviewing budgets, analyzing opportunities, evaluating draw requests and completing site inspections. He’s quickly becoming an expert in the construction draw process as well.

Q: How does a construction draw work with Cetan Funds, and how is it different from a traditional loan disbursement?

Zach & Landon: “The primary difference with how Cetan handles draws is that all draw requests are reviewed & processed entirely in-house, typically within 24–48 hours. Also, we do not typically charge draw or inspection fees on residential rehab or construction projects. We can also work with contractors to pay for down payments and deposits, or pay invoices for our borrowers when the work is completed.”

Q: Is there a limit to how many draws are allowed per project?

Zach & Landon: “We typically allow up to two draws per month to keep the process efficient, but we’re flexible. If your project requires more frequent draws, we can usually accommodate that. There’s no hard limit on the total number of draws over the life of the project.”

Q: Is an inspection required before each draw is approved?

Zach & Landon: “Typically, no. In most cases, we can approve draws based on documentation and photos showing the completed work. If an inspection is needed, it will be done by our loan officer or one of our Principals at no cost to the borrower. The only exceptions are when visual documentation isn’t sufficient or if the project is especially large or complex.”

Q: How long does it take for draws to be processed at Cetan Funds?

Zach & Landon: “We process most draw requests within 24 to 48 hours. Once we receive the request and verify that the work has been completed, we move quickly to release the funds. Our goal is to keep your project moving without unnecessary delays.”

Q: When can a borrower request the first draw?

Zach & Landon: “A borrower can request the first draw anytime after closing, as long as it’s for work that has already been completed. “

Q: How much money will a borrower get with each draw?

Zach & Landon: “Each draw is based on the value of completed work. Our team reviews progress on-site or through documentation to confirm completion of the work included in the draw or that specific milestones have been met. Funds are then released according to the approved draw request, ensuring the loan keeps pace with the actual construction progress.”

Q: What happens if work isn’t completed to the lender’s satisfaction?

Zach & Landon: “Funds may not be advanced for work not completed satisfactorily or up to city/county code.”

Q: What happens if a project runs over budget or behind schedule?

Zach & Landon: “Cetan Funds requires an additional 10% contingency on all construction/rehab loans to provide a margin of safety. Further modifications are considered on a case-by-case basis.”

Q: Can a borrower do their own work on a rehab or construction project?

Zach & Landon: “For major specialty work like electrical, plumbing, or HVAC, a licensed contractor is required. In Oregon, anyone handling new construction must be licensed, bonded, and insured by law. So while borrowers can do many aspects themselves, key parts of the job must be done by qualified professionals and certain ground-up builds must be overseen by someone with a valid CCB license.”

Q: Are draws available for soft costs like permits?

Zach & Landon: “Yes, soft costs such as planning, permits and other city fees can be included in the construction budget.”

Q: Can funds be used for any project-related cost?

Zach & Landon: “Funds must be used strictly for property improvements. They can’t be applied to general business expenses like fuel, administrative costs, or equipment purchases.”

How Cetan Funds Simplifies the Process

As a direct lender managing our pooled private equity fund, we make fast decisions without relying on outside investors. Our construction loans are tailored to your timeline and goals, whether flipping a fixer-upper, finishing a stalled project, or building from the ground up.

Here’s what sets Cetan Funds apart:

-

No Draw Fees: Unlike many lenders, we don’t charge additional fees for draw processing or inspections on most residential projects.

-

Local Insight: We understand Oregon’s building codes and permitting challenges.

-

Flexible Structure: We adjust to your project’s needs, not the other way around.

-

Only Pay for What You Use: Interest accrues only on the money you’ve drawn, not your total loan amount.

A clear, well-managed construction draw schedule is one of the most essential tools for staying on budget, keeping your crew paid, and finishing on time. At Cetan Funds, we’re here to make that process easier, faster, and more transparent.

Are you a real estate investor, builder, or contractor in Oregon or Southwest Washington with a project in mind? We may be able to help. Contact us or visit our Loan Programs page to learn how Cetan Funds can support your real estate success.

Loan Inquiry

For more information on how Cetan Funds can finance your real estate project, please fill out our inquiry form below. We will respond in two business days.

Your Contact Information

Information collected will only be used to evaluate your loan.

Investor Inquiry

For more information about investing in Cetan Income Fund, please fill out our inquiry form below. We will respond in two business days.

Your Contact Information

Information collected will only be used to contact you.

Broker Inquiry

If you have a deal you need help funding or want to inquire about our Broker Referral Program, please contact us below.

Your Contact Information

Information collected will only be used to contact you.

General Inquiry

We’d love to hear from you. Please submit your inquiry below and we will respond in two business days.

Your Contact Information

Information collected will only be used to contact you.

BORROWER FAQs

What is a Private or Hard Money Loan?

Private and hard money loans come in many variations, but most are short-term loans provided by an investor or group of investors when conventional financing is unattainable or undesirable.

Most private lenders and hard money lenders, like Cetan Funds, finance projects like fix and flip rehabs, rental properties, commercial bridge loans, land development, and many other unusual or unconventional properties and projects. A private or hard money loan can help real estate investors, developers, builders, and small businesses grow their portfolios and businesses faster than they could on their own.

Here at Cetan Funds, we empower people to build wealth through real estate.

Why choose hard money vs. bank loans?

Hard money (or private) loans are built for speed and flexibility. Banks often require months of paperwork, strict borrower qualifications, and rigid underwriting standards. At Cetan Funds, we base our lending decisions primarily on the value and potential of the property, not just the borrower’s financial profile. This means we can finance properties and projects banks typically decline due to condition, complexity, or unusual circumstances.

Hard money loans are ideal for time-sensitive opportunities like fix-and-flip projects, new construction, or land development.

Where Does the Money You Lend Come From?

Cetan Funds offers two pooled private equity fund investments for Oregon residents who qualify and accredited investors. Our two funds, called Cetan Income Fund and Cetan Opportunity Fund, serve as the primary source of capital for the loans that Cetan Funds originates.

Rather than matching individual investors to individual loans, or borrowing capital from banks or Wall Street as many hard money lenders do, at Cetan Funds, we manage our own pool of funds. The investors own shares of their fund limited liability company and the principals of Cetan Funds manage the portfolio of loans owned by the fund. All loans are serviced by Cetan Funds. To learn more about the advantages of this structure, please contact us.

What Types of Loans Does Cetan Funds Finance?

We can lend on most commercial and residential property in Oregon and SW Washington if the loan is for business or investment purposes. We provide short-term financing for bare land, land development, new construction, rehabs, and residential and commercial bridge loans.

Do You Lend on Primary or Secondary Residences?

No. We can only lend for business or investment purposes and do not lend on owner-occupied residential properties. Check out our blog to learn more about what we do and what we don’t do.

Where Do You Lend?

We lend exclusively in Oregon and SW Washington because we know the market well and are committed to helping grow our local market. We lend primarily in Western, Southern and Central Oregon with an occasional loan in Southwestern Washington.

Do You Only Look at the Property/Collateral?

While we are primarily a “collateral-based lender,” we do not solely look at the property/collateral. In our experience, who you lend to is just as important as what you lend on.

We strive to build long-term relationships with our borrowers, and we cannot achieve that if we focus solely on their real estate. So, we also take into consideration character, capacity, capital, and other conditions.

Weighing these important factors, which are often overlooked by other private and hard money lenders, helps us accurately measure risks for both our borrowers and our investors while allowing us to offer better all-around results for our clients.

Do You Have Minimum or Maximum Loan Sizes?

How Long Are Your Loans?

We offer loans as short as 3 months and as long as 60 months; however, most of our loans are for 6 to 12 months. Plus, we build in automatic extensions to every loan to ensure borrowers have time to deal with unexpected events and circumstances.

What Are Your Application and Underwriting Requirements?

Cetan Funds loans are customized to fit each specific scenario. Therefore, application and underwriting requirements can often vary depending on the situation. Typically, we require the following:

For Applications:

- Cetan Funds Business Loan Application (online form, link provided by your loan officer)

- Personal financial statements for all loan guarantors (form provided)

- Property/project description

- Summary of construction or investment experience (if applicable)

For Underwriting:

- 2 years of tax returns for all loan guarantors

- 3-6 months of bank statements

- Project/property-specific documentation (such as purchase/sale agreements, lease agreements, business financials, etc.)

- Detailed rehab or construction plans and budgets (if applicable)

Please contact us for more information on the application and underwriting requirements for your specific scenario.

How Fast Can I Get a Loan Decision?

How fast is funding?

We pride ourselves on moving quickly. Loan decisions are typically made within 1–2 business days, and pre-approval can often be issued just as fast. Once approved, we can close and fund in as little as 3–5 business days, depending on the project and documentation. That speed lets you secure capital and act on opportunities without the delays common with traditional lenders.

Can I Get Pre-Approved?

How Fast Can You Fund and Close a Loan?

As quickly as 3-5 days.

What is Your Minimum Down Payment?

What Are Your Interest Rates?

Rates vary depending on the project. Typically, annual interest rates are 10-12%. Interest is only charged on the outstanding balance. Therefore, interest is not charged on construction or rehab funds until they are drawn. So, for most of our short-term construction and rehab loans, borrowers actually incur far less than 10-12% in interest expense. For more information, please contact us.

What Are Your Loan Fees?

Origination fees vary depending on the project. Typically, origination fees are 2-4% of the loan amount. We also charge a $995-$1,495 administrative fee at closing.

Can I Live in the Property While I Have This Loan?

Unfortunately, no. Our borrowers cannot live in the residential properties we finance for them.

The only exception is in very specific commercial loan scenarios. If you wish to get a loan on a property you would like to live in now, or in the future, please contact us so we can help you find a lender for that. We are happy to help.

Can I Pay Off My Loan Early?

Do You Fund Rehab and Construction Loans?

On Rehab or Construction Loans, Do You Charge Interest on the Full Loan Commitment?

No. Interest is only charged on the outstanding balance.

How Do Construction Draws Work With Your Loans?

Construction draws are typically disbursed for work completed, materials purchased, or subcontractor invoices ready to be paid. Borrowers work directly with their loan officer, their main point of contact from start to finish on the project, to submit draw requests up to twice per month.

We do not charge fees for construction draws. Draw requests include a breakdown of the items awaiting reimbursement or payment, evidence showing the completed work or materials on site, and copies of subcontractor invoices or receipts over $2,500-5,000. Draws are typically processed in 24-48 hours.

Do You Fund Loans on Bare Land?

Yes, we provide bare land loans. Each situation is different. Please contact us for details.

Do You Finance Mobile or Manufactured Homes?

What is “Cetan”?

Cetan comes from the Lakota language and means “hawk spirit.” We chose it to represent the values we bring to lending: vision to see opportunities, loyalty in building long-term relationships, and speed in delivering funding when it’s needed most.

Supporting local organizations like the Cascades Raptor Center also helps us honor that connection to hawks and our beautiful raptors in the Pacific Northwest while giving back to the community.