In Oregon’s evolving housing market, builders and investors often face a strategic decision: pursue speculative construction (spec builds) or focus on pre-sold, contract builds designed for individual buyers. Both approaches have merit, but understanding the differences and having the right financing strategy can make all the difference in today’s competitive environment.

At Cetan Funds, we work with builders and investors every day who are navigating this choice. Here’s a look at how spec and pre-sold construction compare, the pros and cons of each, and how the right financing partner can position builders for success.

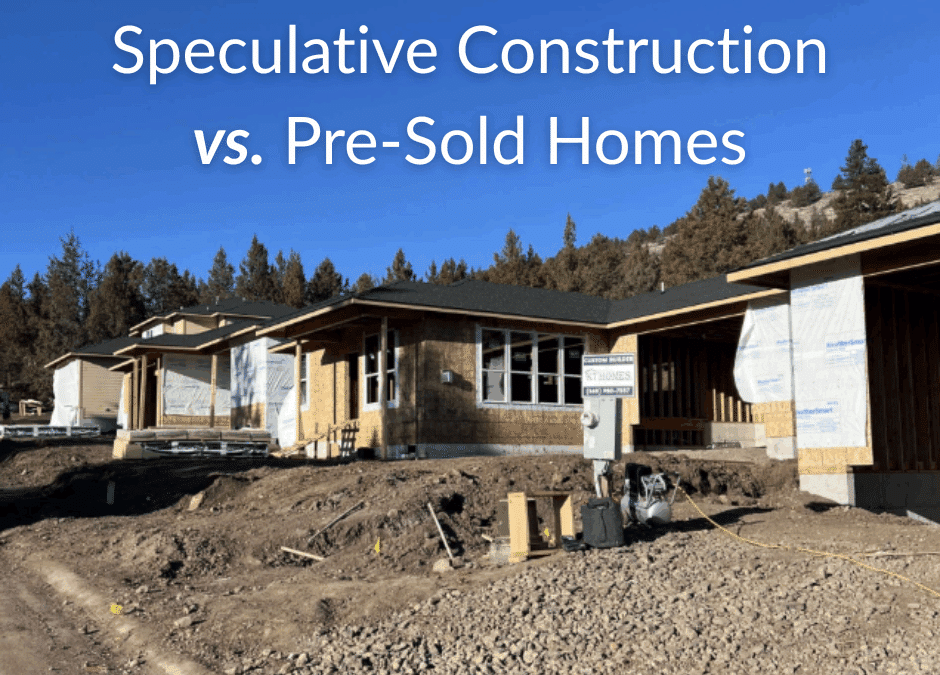

What is the Difference Between Speculative Construction and Pre-Sold Homes?

In real estate, the term “spec build” is short for “speculative build.” This strategy involves constructing a home or small multi-family unit without a buyer secured in advance, with the intent to sell for a profit once completed. The objective is simple: deliver a move-in-ready home that attracts interest and sells quickly once it hits the market. The builder selects popular layouts, features, and finishes with the goal of appealing to a wide range of potential buyers.

Spec homes should not be confused with model homes, which are built solely as display properties to showcase the design and features of homes in a new development and are typically sold only after serving their marketing purpose.

Conversely, pre-sold or contract builds secure a buyer before construction begins. Builders will then work to ensure the floor plans, finishes, and design details are tailored to the buyer’s preferences and customized to their vision.

Both models have clear advantages, but they serve different goals. Spec construction favors speed, efficiency, and creative control, while pre-sold projects prioritize guaranteed sales and predictable cash flow. In this post, we will explore the pros and cons of each approach and show how the right financing partner can set builders up for success.

What are the Advantages of Speculative Construction?

Speculative construction delivers numerous advantages to homebuilders and real estate investors, especially in high-demand housing markets like Oregon. Here are a few that come to mind:

- Creative Freedom and Control: Spec builders have complete say over the home’s design, finishes, and schedule. They can use their market knowledge to build homes that reflect buyer trends, incorporate efficient layouts, and showcase their craftsmanship without waiting on client approvals or navigating change orders.

- Efficiency and Speed: Without client decisions slowing down the process, builders can break ground immediately and move projects forward without interruption. This often results in faster completion timelines, which can be critical in competitive housing markets.

- Economies of Scale: Builders constructing multiple spec homes at once can purchase materials in bulk, keep subcontractors continuously engaged, and streamline scheduling. This reduces per-unit costs and increases profitability.

- Market Opportunity and Higher Profit Potential: When timed well, spec construction can deliver strong margins. Builders who know their local markets can take advantage of rising prices and low inventory to sell quickly at favorable prices.

- Portfolio Growth: Completed spec homes serve as both inventory and marketing tools. Each finished home becomes a showcase for future buyers, strengthening a builder’s reputation and attracting new clients.

What are the Risks of Speculative Construction?

Like most high-reward business strategies, speculative construction comes with risks, and builders must be clear about them from the start. Without a buyer secured in advance, spec builds carry more financial liability during the process than pre-sold builds. Builders are essentially betting that their vision will have broad appeal and sell quickly.

They take on land acquisition, permitting, materials, labor, and financing costs long before the home sells. If the market slows or the property sits unsold, carrying costs such as taxes, insurance, and loan payments can quickly erode profit margins. Staying closely tuned to local real estate trends and buyer preferences is essential to ensure the homes they build match market demand.

That said, this risk is often reduced in high-demand, inventory-constrained markets like Oregon and Southwest Washington, where new homes tend to sell quickly and where we at Cetan Funds focus our lending operations.

Another challenge is financing. Traditional banks are often hesitant to fund speculative projects without a committed buyer. Most banks discontinued construction loan programs for speculative construction long ago. This is where private lenders like Cetan Funds step in, offering the speed, flexibility, and local market expertise builders need to move forward with confidence.

What are the Advantages of Pre-Sold Homes?

The most significant advantage of pre-sold projects is that they minimize financial risk by securing a buyer before construction even begins. Builders know their sale price in advance, which makes cash flow predictable and often makes it easier to secure bank financing, especially if the eventual homeowner purchases the lot upfront and contracts with the general contractor for their custom build.

Pre-sold homes also remove the uncertainty of marketing and selling after completion. There’s no need to stage the property or carry holding costs while waiting for an offer. For many builders, pre-sold projects are also personally rewarding, as they provide an opportunity to collaborate with clients and create a truly custom home that meets their needs.

What are the Risks of Pre-Sold Homes?

Pre-sold or contract builds are a solid option for builders seeking reduced financial risk and greater certainty. However, they come with their own challenges. Working with individual homebuyers introduces a level of complexity not typically found in spec projects. Potential contract adjustments and design revisions, coupled with indecision and schedule disruptions, can delay completion and increase costs.

Builders have less control over the process and must often balance their professional expertise with the buyer’s preferences, even when those preferences reduce efficiency. In many cases, they must compromise on their own design vision to meet client expectations.

Pre-sold builds can also limit profit potential, particularly in fast-moving markets. Because the sale price is locked in early, builders could miss out on market appreciation during construction.

And while pre-sold projects reduce the risk of carrying unsold inventory, they are not entirely risk-free. If a buyer backs out mid-project, the builder may be left with an unfinished home featuring expensive customizations that are difficult to market to other buyers.

Does Speculative Construction Make Sense in Oregon?

Oregon’s housing market continues to evolve, but with the population growing year over year, the state still faces a persistent housing shortage despite new policies designed to boost supply. In markets such as Bend, Eugene, and the Portland metro area, inventory remains tight and prices remain elevated. This environment can create ideal conditions for spec builders who manage costs effectively and select locations strategically.

Spec construction allows builders to deliver much-needed move-in-ready homes into the market quickly. For investors, this means faster sales and potentially higher returns, especially when building multiple homes in small subdivisions to take advantage of economies of scale.

How Can Cetan Funds Help Builders Succeed?

At Cetan Funds, we know the Oregon housing market and specialize in construction and development loans tailored for real estate investors and builders who need flexible, short-term capital to act quickly. Our financing solutions make it possible to take on multiple projects at once, helping builders achieve economies of scale, reduce per-unit costs, and boost overall profitability. We are proud to have financed multiple spec building or development projects, like this recent residential three-home build in Oceanside, Oregon and this exciting new residential four-home project in Klamath Falls.

Here are other ways Cetan Funds is helping builders succeed in Oregon:

- Speed to Market: Our local underwriting process allows for quick approvals and funding, so builders can break ground sooner and reduce carrying costs.

- Flexible Draw Schedules: We align draw schedules with actual construction milestones, improving cash flow and reducing out-of-pocket expenses.

- Tailored Loan Terms: Our 6- to 18-month private loans are ideal for speculative projects and subdivision developments, allowing builders to scale efficiently.

- Local Market Expertise: We know Oregon and Southwest Washington. Our team evaluates projects with on-the-ground insight to help builders choose the right locations.

Both speculative construction and pre-sold projects have a place in today’s residential market. Builders who want stability and guaranteed sales may lean toward pre-sold builds, while those seeking speed, creative freedom, and higher potential returns often choose spec construction.

With the right financing partner, either of these can be a powerful strategy for meeting housing demand and growing your real estate business.

At Cetan Funds, we’re committed to helping Oregon builders and investors take advantage of market opportunities, move quickly, and maximize returns. If you are considering your next project, we invite you to connect with us. Together, we can find the financing solution that helps you bring more homes to the communities that need them most.

Loan Inquiry

For more information on how Cetan Funds can finance your real estate project, please fill out our inquiry form below. We will respond in two business days.

Your Contact Information

Information collected will only be used to evaluate your loan.

Investor Inquiry

For more information about investing in Cetan Income Fund, please fill out our inquiry form below. We will respond in two business days.

Your Contact Information

Information collected will only be used to contact you.

Broker Inquiry

If you have a deal you need help funding or want to inquire about our Broker Referral Program, please contact us below.

Your Contact Information

Information collected will only be used to contact you.

General Inquiry

We’d love to hear from you. Please submit your inquiry below and we will respond in two business days.

Your Contact Information

Information collected will only be used to contact you.

BORROWER FAQs

What is a Private or Hard Money Loan?

Private and hard money loans come in many variations, but most are short-term loans provided by an investor or group of investors when conventional financing is unattainable or undesirable.

Most private lenders and hard money lenders, like Cetan Funds, finance projects like fix and flip rehabs, rental properties, commercial bridge loans, land development, and many other unusual or unconventional properties and projects. A private or hard money loan can help real estate investors, developers, builders, and small businesses grow their portfolios and businesses faster than they could on their own.

Here at Cetan Funds, we empower people to build wealth through real estate.

Why choose hard money vs. bank loans?

Hard money (or private) loans are built for speed and flexibility. Banks often require months of paperwork, strict borrower qualifications, and rigid underwriting standards. At Cetan Funds, we base our lending decisions primarily on the value and potential of the property, not just the borrower’s financial profile. This means we can finance properties and projects banks typically decline due to condition, complexity, or unusual circumstances.

Hard money loans are ideal for time-sensitive opportunities like fix-and-flip projects, new construction, or land development.

Where Does the Money You Lend Come From?

Cetan Funds offers two pooled private equity fund investments for Oregon residents who qualify and accredited investors. Our two funds, called Cetan Income Fund and Cetan Opportunity Fund, serve as the primary source of capital for the loans that Cetan Funds originates.

Rather than matching individual investors to individual loans, or borrowing capital from banks or Wall Street as many hard money lenders do, at Cetan Funds, we manage our own pool of funds. The investors own shares of their fund limited liability company and the principals of Cetan Funds manage the portfolio of loans owned by the fund. All loans are serviced by Cetan Funds. To learn more about the advantages of this structure, please contact us.

What Types of Loans Does Cetan Funds Finance?

We can lend on most commercial and residential property in Oregon and SW Washington if the loan is for business or investment purposes. We provide short-term financing for bare land, land development, new construction, rehabs, and residential and commercial bridge loans.

Do You Lend on Primary or Secondary Residences?

No. We can only lend for business or investment purposes and do not lend on owner-occupied residential properties. Check out our blog to learn more about what we do and what we don’t do.

Where Do You Lend?

We lend exclusively in Oregon and SW Washington because we know the market well and are committed to helping grow our local market. We lend primarily in Western, Southern and Central Oregon with an occasional loan in Southwestern Washington.

Do You Only Look at the Property/Collateral?

While we are primarily a “collateral-based lender,” we do not solely look at the property/collateral. In our experience, who you lend to is just as important as what you lend on.

We strive to build long-term relationships with our borrowers, and we cannot achieve that if we focus solely on their real estate. So, we also take into consideration character, capacity, capital, and other conditions.

Weighing these important factors, which are often overlooked by other private and hard money lenders, helps us accurately measure risks for both our borrowers and our investors while allowing us to offer better all-around results for our clients.

Do You Have Minimum or Maximum Loan Sizes?

How Long Are Your Loans?

We offer loans as short as 3 months and as long as 60 months; however, most of our loans are for 6 to 12 months. Plus, we build in automatic extensions to every loan to ensure borrowers have time to deal with unexpected events and circumstances.

What Are Your Application and Underwriting Requirements?

Cetan Funds loans are customized to fit each specific scenario. Therefore, application and underwriting requirements can often vary depending on the situation. Typically, we require the following:

For Applications:

- Cetan Funds Business Loan Application (online form, link provided by your loan officer)

- Personal financial statements for all loan guarantors (form provided)

- Property/project description

- Summary of construction or investment experience (if applicable)

For Underwriting:

- 2 years of tax returns for all loan guarantors

- 3-6 months of bank statements

- Project/property-specific documentation (such as purchase/sale agreements, lease agreements, business financials, etc.)

- Detailed rehab or construction plans and budgets (if applicable)

Please contact us for more information on the application and underwriting requirements for your specific scenario.

How Fast Can I Get a Loan Decision?

How fast is funding?

We pride ourselves on moving quickly. Loan decisions are typically made within 1–2 business days, and pre-approval can often be issued just as fast. Once approved, we can close and fund in as little as 3–5 business days, depending on the project and documentation. That speed lets you secure capital and act on opportunities without the delays common with traditional lenders.

Can I Get Pre-Approved?

How Fast Can You Fund and Close a Loan?

As quickly as 3-5 days.

What is Your Minimum Down Payment?

What Are Your Interest Rates?

Rates vary depending on the project. Typically, annual interest rates are 10-12%. Interest is only charged on the outstanding balance. Therefore, interest is not charged on construction or rehab funds until they are drawn. So, for most of our short-term construction and rehab loans, borrowers actually incur far less than 10-12% in interest expense. For more information, please contact us.

What Are Your Loan Fees?

Origination fees vary depending on the project. Typically, origination fees are 2-4% of the loan amount. We also charge a $995-$1,495 administrative fee at closing.

Can I Live in the Property While I Have This Loan?

Unfortunately, no. Our borrowers cannot live in the residential properties we finance for them.

The only exception is in very specific commercial loan scenarios. If you wish to get a loan on a property you would like to live in now, or in the future, please contact us so we can help you find a lender for that. We are happy to help.

Can I Pay Off My Loan Early?

Do You Fund Rehab and Construction Loans?

On Rehab or Construction Loans, Do You Charge Interest on the Full Loan Commitment?

No. Interest is only charged on the outstanding balance.

How Do Construction Draws Work With Your Loans?

Construction draws are typically disbursed for work completed, materials purchased, or subcontractor invoices ready to be paid. Borrowers work directly with their loan officer, their main point of contact from start to finish on the project, to submit draw requests up to twice per month.

We do not charge fees for construction draws. Draw requests include a breakdown of the items awaiting reimbursement or payment, evidence showing the completed work or materials on site, and copies of subcontractor invoices or receipts over $2,500-5,000. Draws are typically processed in 24-48 hours.

Do You Fund Loans on Bare Land?

Yes, we provide bare land loans. Each situation is different. Please contact us for details.

Do You Finance Mobile or Manufactured Homes?

What is “Cetan”?

Cetan comes from the Lakota language and means “hawk spirit.” We chose it to represent the values we bring to lending: vision to see opportunities, loyalty in building long-term relationships, and speed in delivering funding when it’s needed most.

Supporting local organizations like the Cascades Raptor Center also helps us honor that connection to hawks and our beautiful raptors in the Pacific Northwest while giving back to the community.